The idea of providing a periodic, unconditional cash transfer to all residents of a country – a universal basic income – has rapidly gained traction in recent years. However, the debate about basic income often seems curiously divorced from the wider debate about the expansion of social security systems, writes Rasmus Schjoedt.

For example, the debate about the potential for a basic income in India has so far neglected what seems like an obvious argument: that making India’s existing tax-financed social security programmes universal would be an important first step towards a universal basic income.

A universal basic income is one way of expanding social security systems and should be seen in relation to other initiatives and international frameworks in this area. As the UN Special Rapporteur on extreme poverty and human rights, Philip Alston writes in his recent report on basic income: ‘The debates over social protection floors and basic income need to be brought together… if it is recognized that basic income is not an idea that can be achieved in a single leap, there could be no better and more elaborate and widely supported programme than that of the social protection floor.’ (Alston 2017).

The concept of ‘Social Protection Floors’ is enshrined in the International Labour Organisation’s Social Protection Floors Recommendation, 2012 (No. 202), which is the cornerstone of the internationally defined normative framework for social security systems across the world. Through the social protection floors concept, the Recommendation provides the minimum core content of the human right to social security. According to Recommendation 202, social protection floors should guarantee as a minimum basic income security for children, persons in active age and older persons, as well as effective access to health care.

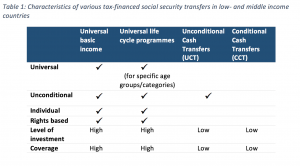

This normative framework underpins global efforts to expand access to universal social security programmes. Universality in this context means that welfare states are developed that provide services to entire populations, including for example child benefits for all families with children, rather than only for those deemed to be ‘poor’. Based on this normative framework, social security systems should therefore be measured by how well they provide coverage for entire populations across the whole of a person’s lifecycle.

Recent decades have seen an impressive expansion of social security transfers in low- and middle-income countries. However, there are large differences between these programmes, with some more in line with the principle of the right to social security than others: Conditional and unconditional cash transfer programmes are poverty targeted household transfers, which are not rights-based. On the contrary, life cycle programmes, such as pensions, child grants and disability benefits, are individual entitlements, and many are universal.

Conditional and unconditional cash transfer programmes compare unfavourably with a universal basic income: first of all, they are targeted at households, not individuals; second, they are targeted at ‘the poor’, rather than being offered to everyone; third, related to the above point, these programmes are not rights-based but are, instead, provided as a form of charity, and; fourth, they often come with conditions attached.

Finally, government spending on these programmes is generally low, and they cover relatively small parts of the population (and usually miss the majority of their target population). This is important, because high levels of spending on programmes that reach a broad section of the population is necessary for social security to contribute to more equitable societies, rather than just alleviating the most extreme poverty. And, spending and coverage are tightly connected, not just because expanding coverage requires increasing spending, but also the other way around: high coverage rates are essential for creating the broad support in the population that is necessary to create the political will to increase spending.

But can low- and middle-income countries afford to implement social security programmes that are aligned with the right to social security for all? The answer is yes, and many countries are already doing it, by investing in universal life cycle social protection schemes such as old age pensions, child grants and disability benefits. These programmes have much more in common with a universal basic income since they are individual, unconditional, rights-based and often universal.

Despite their advantages, lifecycle social security schemes usually do not attract the same attention as poverty-targeted cash transfer programmes. The latest large review of cash transfers by the ODI included a review of research covering 56 different programmes. Out of these, 45 were CCTs/UCTs and only 4 were old age pensions. The poverty-targeted programmes also tend to receive much more media attention.

This is despite the fact that the lifecycle programmes are usually more popular than poverty targeted programmes, have stronger political support and have expanded significantly among low- and middle-income countries in recent decades: many low- and middle income countries now have a wide range of lifecycle schemes and invest significant amount of money in them.

Countries with growing lifecycle systems include, for example, Mauritius, South Africa, Uzbekistan, Mongolia, Georgia, Namibia and Nepal. In Brazil, the national old age, disability and unemployment benefits, although not universal, are much more significant than the much-hyped Bolsa Familia programme, a poverty-targeted household benefit. Mauritius has had a universal pension since the 1950s, which now co-exists with a universal disability benefit and a range of other social security schemes while Nepal has been quietly building an impressive universal social protection system since the mid-1990s. This year Kenya launched a tax-financed universal pension for everybody aged 70 years and above; Uganda already have a pension that is universal in some parts of the country, while Zanzibar introduced a universal pension in 2016.

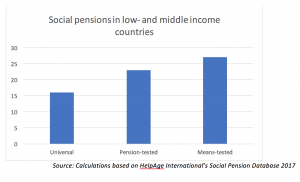

Altogether, 67 low- and middle income countries now have social pensions. Out of these, sixteen have universal pensions, while another 23 provide universal access to everybody except those already benefitting from a contributory pension.

The most likely pathway towards a universal basic income in low- and middle-income countries, is, therefore, to start with universal lifecycle transfers, in particular universal old age pensions, child benefits and disability benefits. This would gradually increase spending in a way that is popular among both politicians and populations, and would introduce the central principle of universality in the social security system.

As Martin Ravallion has argued, even if a universal basic income is not yet feasible in many countries, a more universal approach would create better social policies. As the UN Special Rapporteur, Philip Alson, points out, universal lifecycle programmes can be seen as ‘partial’ basic incomes, effectively providing a universal basic income for people at different stages of their lives.