Indonesia is one of the few countries in South-East Asia not to have a social pension. The only pensions available are financed from social insurance and, in the main, are received by former civil servants. In fact, only around 15 per cent of older people can currently access a pension, and yet more than 20 million people are aged 60 years and over, the majority being women, writes Stephen Kidd.

A comprehensive old age pension system is becoming an urgent necessity for Indonesia. The highest poverty rates nationally are found among older people, who are becoming increasingly isolated: already 56 per cent of older women are widowed while 15 per cent live alone, with the number rising. The situation is only going to worsen given the fact that Indonesia is an ageing society: while around 8.5 per cent of the population is currently aged 60 years and above, this will rise to 13 per cent by 2030.

But, things may be about to change. Last week, TNP2K – a think-tank based in the Vice-President’s office – held a workshop to discuss a range of options for achieving wider pension coverage. It was attended by key people from across government. Development Pathways was privileged to participate and present some of the work we have been undertaking, in collaboration with TNP2K and MAHKOTA, a social protection policy program in Indonesia funded by the Australian Government.

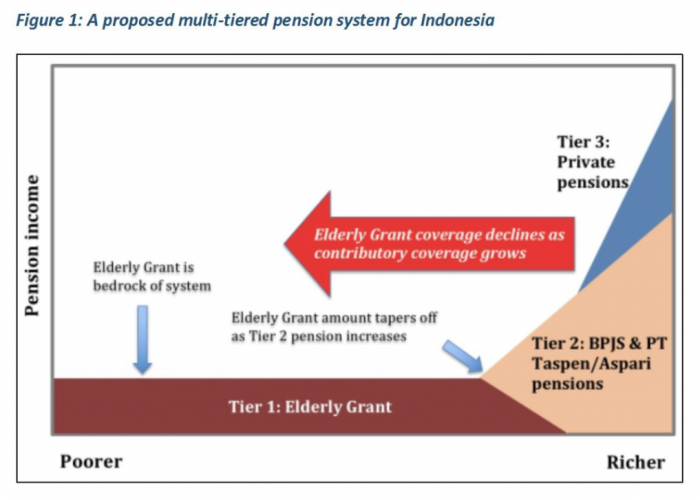

The workshop proposed a multi-tiered pension system for Indonesia, with the first Tier a social pension – currently known as the ‘Elderly Grant’ – which would guarantee pension coverage for all Indonesians (see Figure 1). Over time, as coverage of older people by the social insurance schemes expands, the social pension will shrink, thereby reducing the cost, but everyone will always be able to access a pension once they reach the age of eligibility.

One option for the social pension would be to give every older person aged 65 years and above IDR 600,000 (US$43) per month. This is an amount that is – when measured as a percentage of GDP per capita – below the average found internationally in inclusive social pension schemes, so it is not unreasonable. It would also require an investment of only 0.68 per cent of GDP, which again is relatively modest when compared to what many other low and middle-income countries invest. For example, Nepal, one of the poorest countries in Asia, is investing around 1.3 per cent of GDP in a social pension for everyone aged 65 years and above.

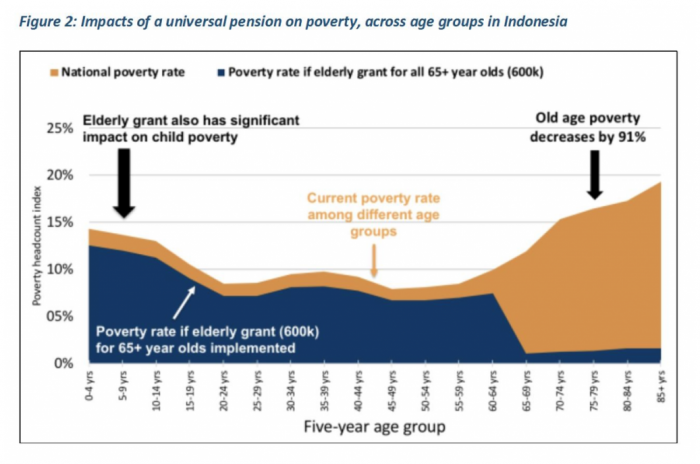

As Figure 2 shows below, this social pension option would almost eliminate old age poverty, reducing it by 91 per cent. It would also have significant impacts on child poverty, since it is well-established that pensioners around the world prioritise supporting their grandchildren. Importantly, such an Indonesian pension would help the Government to achieve its poverty reduction targets by reducing the national poverty rate from 10.6 per cent to 8.4 per cent (and even more if multipliers are taken into account). A more comprehensive discussion on the proposed pension can be found in a briefing paper produced by TNP2K (see here).

Universal pensions are not unknown in Indonesia. There is at least one district – Aceh Jaya – that is currently implementing a universal social pension, financed from local resources. And, as can be read here, the programme has had significant impacts, despite only giving older people IDR 200,000 (US$15) per month. MAHKOTA has put together a great video on the scheme.

It’s the right time to propose an inclusive pension for Indonesia. Next year Indonesia has Presidential elections and it is well-established that the offer of a universal pension can win an election. Around 43 per cent of Indonesia’s electorate are either aged 50 years and above, or live with someone aged at least 60 years, so it is an issue that cannot be ignored. The first Presidential candidate to promise an Indonesian pension is likely to be the winner. Keep reading our blogs and we will update you!