Author: Stephen Kidd

I started working full-time on social security – often referred to as social protection in international development – just over 20 years ago. At the time, social security was regarded as an innovation in international development circles although, in most high-income countries, it was already a mainstay of social policy and an essential public service. Looking back, it seems strange that so many ‘experts’ in international development hadn’t realised that the easiest way to tackle poverty was to just give people cash and that the right of everyone to access social security had been guaranteed as far back as 1948, within the Universal Declaration of Human Rights.

Over the past 20 years, interest in social security within international development circles has sky rocketed. Rarely a week goes by when Ugo Gentilini – in his incredibly useful newsletters – does not announce at least 10 new papers on the topic. The evidence on the positive impacts of social security continues to grow and the case for countries investing in social security seems irrefutable.

At global level, there is a consensus that universal social security must be implemented in all countries. It is embedded in a range of international agreements, such as the ILO’s Recommendation 202/2012 on Social Protection Floors and the Sustainable Development Goals. Many organisations have come together behind the call for Universal Social Protection by 2030 although, as we’ve highlighted, at least one highly influential global development partner within the USP2030 alliance has strangely interpreted universal to mean poverty-targeted! Baby steps: they’ll surely get there soon (and hopefully before 2030)!

However, progress on the ground has not been so good. While there have been some great successes over the past two decades with some low- and middle-income countries implementing large-scale universal schemes, we’ve now identified at least 89 universal coverage schemes in low and middle-income countries – still, far too many people are excluded from social security. Coverage is particularly limited in low- and lower middle-income countries: according to the ILO, only 7 per cent of people can access a benefit in low-income countries and only 21 per cent in lower middle-income countries.

Unfortunately, over the past 20 years, an ideological struggle on social security has been raging. On the one hand are those committed to a small state and low taxation – i.e. neoliberals – who argue that benefits should be directed to the poorest members of society. By only supporting the poorest, the costs to the state can be kept low. Yet, as we have shown, due to high errors, poverty targeting ensures that most of the poorest members of society miss out on social security.

On the other hand, there are those who see the value of a larger state, higher government revenues and effective redistribution and, therefore, argue for universal social security benefits to address the risks we all face across the lifecycle. They understand that the only effective means of delivering social security to tackle poverty and ensure that all the poorest members of society can access a minimum level of income security is through a universal lifecycle social security system.

This ideological war has impeded global progress in building universal social security systems. A constant refrain from our neoliberal friends is that countries cannot afford to build universal social security systems. In fact, if I were given a penny for each time I’d heard the phrase ‘there is no fiscal space,’ I’d be a wealthy man. Yet, nothing could be further from the truth. The absence of fiscal space for universal social security is a political choice. Of course, this does not mean that comprehensive universal social security systems could be introduced overnight. But, they certainly could be built over a period of 10 to 20 years. We need to remember that high-income countries built their universal systems over decades, and we should not expect anything different in low- and middle-income countries.

In our recently released paper on the cost of building social security systems across 118 low- and middle-income countries, we have shown that it would cost an average of 3 per cent of cumulative GDP to introduce universal systems immediately. This is too high a cost in most countries, although in some that have already made good progress in building universal systems, the cost would be much lower.

However, if countries were to build universal systems gradually, over 10-20 years, the cost falls considerably. We show how countries could slowly introduce a range of lifecycle schemes – focusing on old age, disability, child, maternity and caregivers’ benefits – by gradually expanding coverage but consistently maintaining the universality of provision. For example, we show how old age pensions could begin with a higher age of eligibility, which could fall over time; and, in the case of child benefits, countries could commence with young children and, by not removing recipients until they reach 18 years of age, the benefits would eventually become universal for all children. In our costings, we also take into account current spending on similar schemes within countries so that we, in effect, cost out the financing gap for introducing universal social security

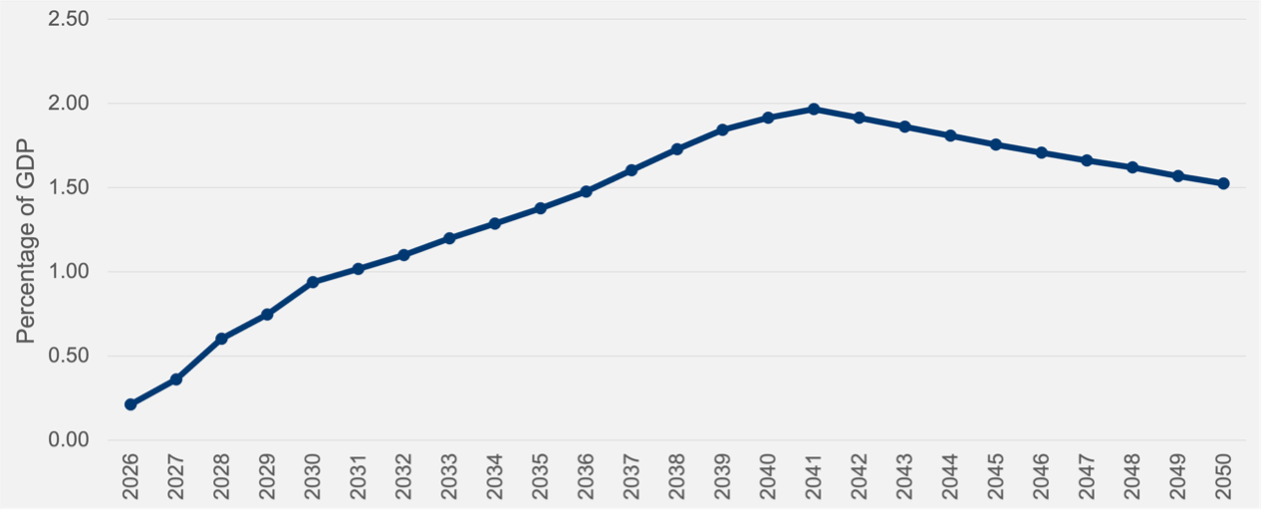

Figure 1 shows the weighted average financing gap for gradually building comprehensive, universal social security systems across the 118 countries in our study. Countries could start building their systems in 2026 by introducing a universal old age pension at only 0.2 per cent of GDP. By 2041, the maximum cost of closing the coverage gap would be reached, at just under 2 per cent of GDP. The additional funding required each year between 2026 and 2041 would be only 0.12 per cent of GDP, a marginal cost in most countries.

Figure 1: The weighted average financing gap to gradually build comprehensive social security systems across 118 low- and middle-income countries

Importantly, given that the ILO dismayed many onlookers – though not our neoliberal friends – by claiming that it would cost 19.8 per cent of GDP to build universal social security systems across low-income countries, we estimate that it could cost as little as 1.56 per cent of GDP if schemes are introduced gradually over 10-20 years in the world’s poorest countries. Again, this is very affordable since the annual increases in investment would be minimal.

Our costings show that universal social security is feasible everywhere, as long as political leaders make the right policy choices. The global commitment to increase social security coverage by only 2 percentage points per year – as set out in the Doha Political Declaration of the 2025 World Social Summit – is far too pessimistic and does not align to the fiscal reality that universal social security systems are possible everywhere, as long as countries introduce them gradually. Bizarrely, USP2030 endorsed the target of 2-percentage points despite the fact that, in a country with no child benefit, this would mean that it would take 50 years to build a universal child benefit. Perhaps a change in name to USP2080 might better reflect the true ambition of the alliance!

Imagine if countries had realised, 20 years ago, that they could build comprehensive universal social security systems within 20 years. Universal social security systems would now be in place across the world. Unfortunately, the dominance of neoliberal thinking in social security ensured that the belief ‘there is no fiscal space’ prevailed, resulting in many countries building small, ineffective poverty-targeted benefits that are little loved even within their own countries. As a result, billions of people – including most of the world’s poorest citizens – have missed out on accessing the social security schemes that could have transformed their lives. These have been 20 wasted years.

Our study shows that universal social security is within our grasp. It is affordable and could be progressively realised using the principle of universality. All countries can take the popular choice of building universal social security systems at minimal cost, thereby tackling poverty, delivering human development, strengthening national social contracts and helping drive economic growth. The popular choice, however, is still a political choice. Let’s hope that politicians make the right choice so that we don’t look back in 2045 and see the same lack of ambition that has failed us over the past 20 years. Let’s not let history repeat itself.